2025 Performance Update & Thoughts On The Current Market Environment

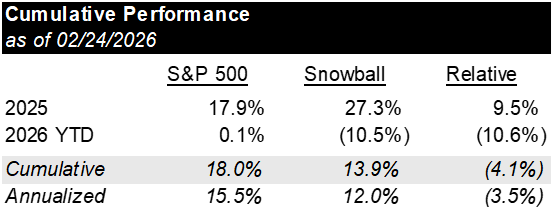

2025 & 2026 YTD Performance

I ended 2025, my first full year of tracking this "Snowball Portfolio" up ~27.5% vs. ~18% for the S&P 500 index – outperforming my benchmark by ~9.5 points.

Solid year, except for the fact I've given back all of 2025's outperformance in the first couple months of trading in 2026.

The past few weeks have been a wild time in markets (my portfolio is down ~10%), with significant underlying market volatility masked by a relatively stable index (+10bps YTD). Below I walk through some of the more interesting phenomena I've observed recently and my thoughts on the current environment. I start with the timely and attempt to zoom out to the structural.

Note: I'm not providing an exact breakdown of my portfolio in this post because market volatility has been presenting significant opportunities to trim winners and add to losers in the current environment, therefore, considering my position sizing is somewhat dynamic right now, it likely makes more sense to reveal more about my current portfolio when the dust has settled a bit. I hope to do this at least once a year. With that said, I find AMZN, MSFT, UBER, APO, ROP, MLM, META, AYI, and GOOG (although it has gotten more expensive recently) attractive, and have the bulk of my capital concentrated in these businesses.

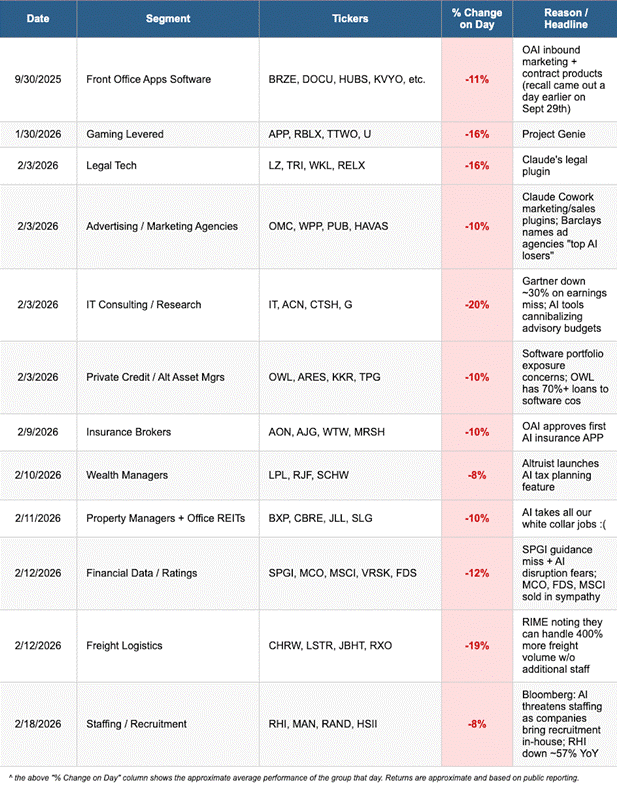

Rolling AI Headline Risk & The HALO Trade

For the past several months, different industries have been selling off as the market attempts to grapple with the implications of AI. Each new product launch/announcement from the frontier labs, weak earnings print from a potential “AI loser,” or thematic AI blog post triggers a fresh round of selling in a new industry. The table below captures the rolling timeline. Apologies if I'm missing any as it's been tough to keep up with them all:

The sell-offs above occurred before the thematic blogger "Citrini Research" posted a pessimistic 2028 thought exercise calling for a "global intelligence crisis," which has since driven intra-day sell-offs in software (evergreen), DASH, V/MA, the alternative asset managers, the OTAs, and the broader market.

What's happening is a market-wide pattern of “shoot first, ask questions later” (no comment as to whether or not that’s appropriate, just highlighting the fact it is happening). Investors are having an extraordinarily difficult time underwriting tail risks. If a business has physical infrastructure or a real-world connection, it feels safe. Otherwise, "high likelihood of being well-positioned" isn't good enough. The result is what some are calling the "HALO trade" (Hard Assets, Low Obsolescence), with Energy (+23%), Materials (+16%), Staples (+14%), Industrials (+13%), Real Estate (+8%), and Utilities (+7%) leading the market year-to-date (along with semis).

It's worth noting the irony: the HALO trade is almost the exact inverse of the COVID trade. In 2020, the consensus was that the physical world was impaired and the digital economy was where you needed to concentrate capital: buy software, buy e-comm, buy payments… short anything tied to real-world activity. Investors piled into asset-light businesses with recurring digital revenues and fled from anything requiring physical presence. In 2026, the trade has flipped. Physical infrastructure, real assets, and labor-intensive businesses are the safe havens, while digital-first, asset-light businesses are priced as existentially threatened. The same categories of stocks that were "COVID winners" are now "AI losers," and the "COVID losers" have become the HALO darlings.

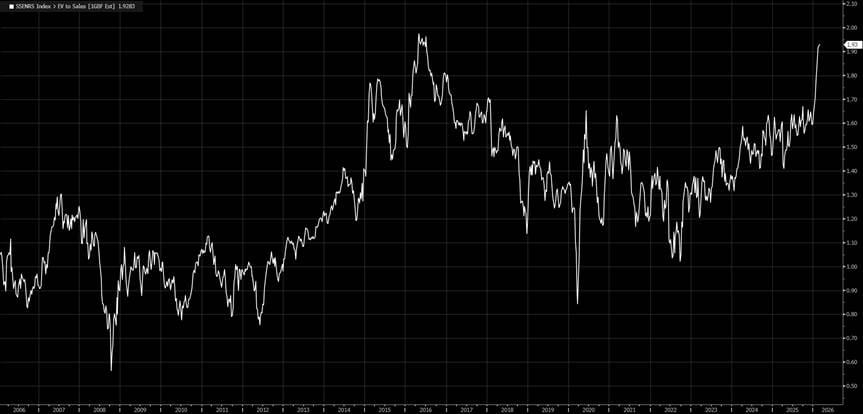

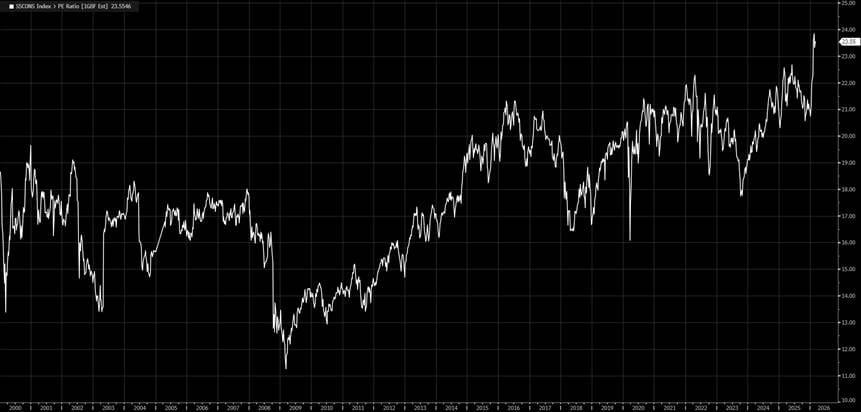

The valuation inversions this rotation has produced are remarkable. The GICS Industrials sector now trades at 27.5x forward earnings (100th percentile vs. its own history). Consumer Staples trade for 25.0x (for ~5–6% EPS growth). Energy trades for 21.0x (or an ATH ~2x EV/Sales; the negative oil price during COVID made earnings estimates unintelligible during that period so I’m using a sales multiple).

All of these compared to the S&P 500 Index at ~21.5x earnings.

S&P 500 Energy Sector | EV/NTM Sales (2006 – Present)

S&P 500 Consumer Staples Sector | P/NTM Earnings (2000 – Present)

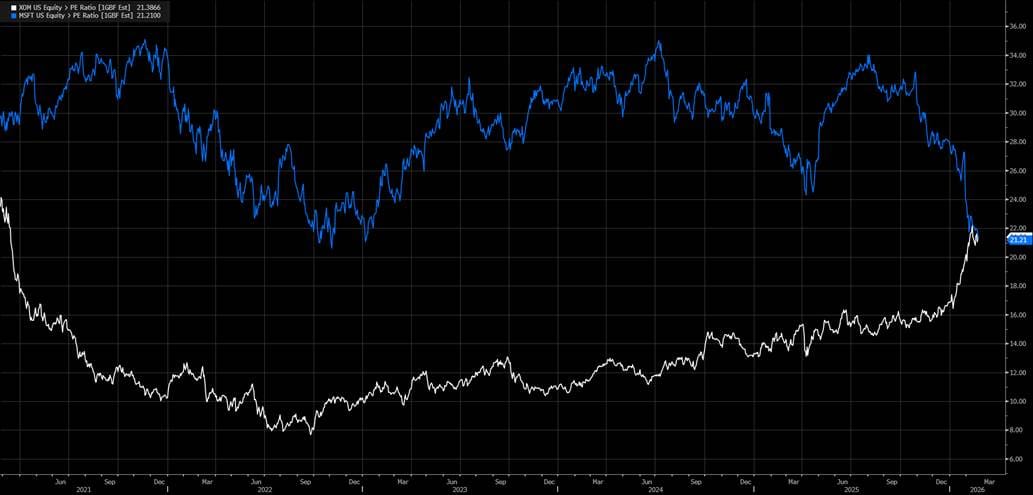

The chart below may best sum up the current environment: Microsoft now trades at a lower forward earnings multiple than Exxon Mobil.

The valuation premium for non-capital-intensive businesses over capital-intensive ones has been collapsing, reversing what many understood as a fixture of valuation ("you'd rather require no incremental capital to grow"). Whether this represents a durable regime shift or a fear-driven overshoot is, of course, the key investment question. But the speed and uniformity of the rotation is likely a market-structure phenomenon vs. a completely fundamental one, as entire sectors are being repriced on narrative.

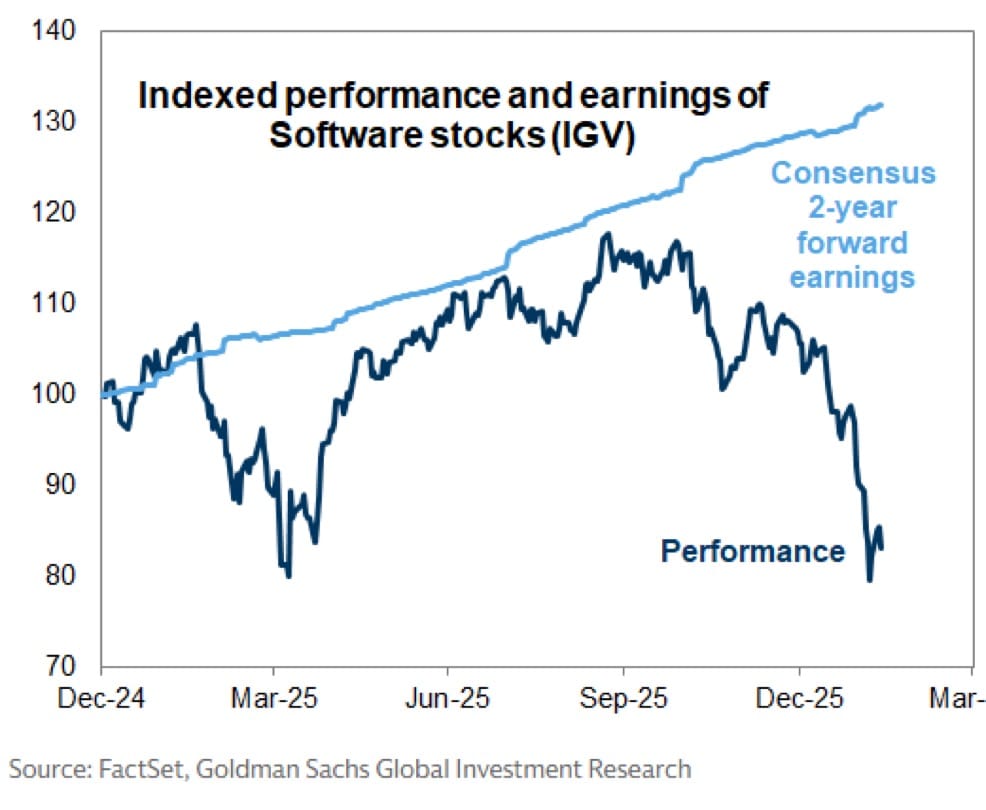

While software is the poster child for “AI will replace this,” it’s worth pointing out that forward earnings estimates have actually been rising as we exit earnings season. More than 100% of the recent drawdown has been due to multiple compression. That compression may very well end up being partially or fully justified, but I thought it was interesting to note we haven’t yet seen collective earnings estimates coming down for the “AI losers.”

Single-Stock Volatility

We continue to see extraordinary levels of single-stock volatility, even as the index itself sits near all-time highs. BofA data from the Q3 2025 earnings season highlights that beats were rewarded slightly below historical averages, while misses were punished significantly more than usual. With ~80% of the S&P 500 now having reported Q4 2025 results, this asymmetry has continued – and gotten more acute.

The numbers are interesting: in Q3 2025, companies that missed on both EPS and sales suffered an average -4.6% one-day relative move and -13.3% move from the start of reporting season to five days after the print. This is a market with no patience for disappointment; likely consistent with the marginal investor base operating on three-week to three-month time horizons and managing to tight drawdown limits (more on this below).

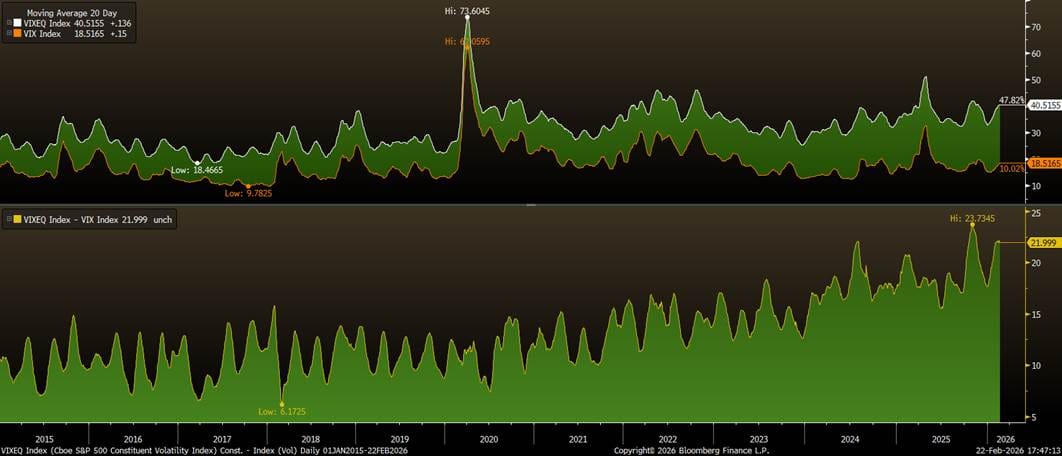

Another way to measure single-stock volatility is to compare the VIX (30-day implied vol at the index level) to the VIXEQ (30-day implied vol of all index constituents). The divergence is striking and historically unprecedented. Pre-COVID, the average S&P 500 stock had implied volatility of roughly 23–25 while the index ran at 13–15 vol points. Today, the average stock has implied volatility north of 40 (approximately 75% more volatile than pre-COVID) while index vol itself has moved up only modestly towards the high teens. We have never seen a higher ratio of single-stock volatility to index-level volatility.

And outside of 1999/2000, we haven't seen such a significant degree of single-stock blowups with the index so near all-time highs (defined as 115+ members of the S&P 500 suffering a one-day, 7%+ sell-off during any rolling 8-day window).

Changing Market Microstructure (Passive + Retail + Quants/Multi-Managers… w/ Lack Of Independent Thought Adding Fuel)

To use technical terminology – something weird is going on. While we can't ascribe direct cause and effect (markets are dynamic, constantly evolving ecosystems), I believe there are compounding structural factors producing this abnormal market behavior. Over the past ~20 years, three primary forces have fundamentally altered the composition of (i) who is setting prices, (ii) on what time horizon, (iii) with what risk tolerance, (iv) and how independently they all form their conclusions.

The Rise of Passive

While "the rise of passive" has been a persistent boogeyman that many active managers have used to explain away underperformance, the persistent flows into passive funds (which surpassed 50% of U.S. equity fund AUM in 2024) are likely contributing to a less efficient market.

The logic is straightforward. No market can be 100% passive, because someone must set prices. And common sense implies that all of the "weirdness" doesn't arrive at the last 1% -- i.e., no effect at 99% passive and then complete distortion at 100%. There has been an incredible amount of ink spilled on this topic, with ardent supporters on both sides. But I think it is naive to believe that such a sea-change in market structure has generated no change in price efficiency.

Cliff Asness, the co-founder of AQR, addressed this directly on Odd Lots in November 2025 discussing his recent paper “The Less Efficient Market Hypothesis.”

“I am not a passive hater... But here's what we know: the whole world cannot be passive. We had Jack [Bogle] (founder of Vanguard) on our podcast, and he absolutely agreed: everyone can't be passive. Now, of course, being Jack Bogle, he thinks at that point the marginal investor should still move to passive. But he recognizes the obvious fact that if one hundred percent of the people are not looking at prices, nobody's looking at prices. Who's figuring out if Nvidia is worth more or less than the corner drug store. The market gets very weird there. We don't even understand what happens. It's a singularity… I think fewer people thinking about prices, fewer people willing to take the other side when things get a little crazy – if one side really starts to get crazy, there are fewer people out there. That has to exacerbate these swings."

The Rise of Retail

After approximately 40 years of declining retail participation, with individual ownership of corporate equities dropping from ~75% to ~35% between 1970 and 2010, retail ownership of equities is back on the rise. Retail investors have now reached ~21% of total trading volume, up from ~10% in 2010.

The reasons for this uptick are multiple: the rise of free trading via payment-for-order-flow schemes, proliferating app-based trading interfaces, three rounds of COVID stimulus checks delivered while people were locked in their homes, and an under discussed rising Gen-Z financial nihilism that has blurred the line between investing and gambling. Without diving into the extensive academic research on retail investors (who tend to be more risk-seeking, tend to underperform, tend not to understand the risks they're taking, and tend to chase momentum) a market seeing increased retail participation is almost certainly a less efficient market.

On this topic as well, Asness was characteristically blunt:

"I hate this because I sound very elitist when I diss on retail, but there's a lot of academic work that shows retail on net loses. 'On net' is important – they go through periods where they win, they go through periods where they win a lot. You know, if you buy a meme stock and it triples tomorrow, you don't always lose. But on average, retail transfers money to Wall Street and to institutions. So if they are a bigger force in markets, you're going to have more of that going on. And it jibes perfectly, because that would raise the opportunity – if they're generally on the wrong side of things, but there are more of them, many more of them than there used to be, they can be right even if they're wrong on the facts. They can be right on the numbers for longer than they used to be."

Reduced Influence of Fundamental Funds

Even among the “active, institutional investors,” the data on who is actually trading is revealing. Counterpoint Global / Michael Mauboussin show that the total share of U.S. equity trading volume attributable to fundamental funds has shrunk from 23.4% in 2010 to 14.8% in 2025. Meanwhile, the combined volume share from quant funds and retail investors has increased from ~30% to over 60% per Empirical Research.

By definition, this results in a materially reduced fraction of equity trading volume being driven by long-term oriented investors.

Ricky Sandler (of Eminence Capital), described the shift on a recent episode of Masters in Business with Barry Ritholtz:

"Fifteen years ago, the marginal price setter was a bottom-up investor. Markets were 25% passive and 75% active, and most active investors did bottom-up research. Fast forward to today, that 25% index is now 60%. So David's right about how big indexing has become… they are accepting prices. But the bigger change is also that the remaining 40%, relative to the old 75%, is not bottom-up stock pickers. It's quant investors, it's pod shops trying to make money in every one-, two-, three-week or two-month period. It's thematic investors, systematic investors, retail investors... We see all this investing done in what I call blunt-instrument investing. People talk about the theme du jour — 'we want to buy AI,' 'the GLP-1 losers,' 'the GLP-1 winners.'… How about a business? How about an individual company?"

Shrinking Time Horizons Among Remaining Fundamental Active Managers

Even within the universe of capital that does fundamental work, time horizons have compressed dramatically. Multi-manager platforms have delivered strong risk-adjusted returns over the past decade and attracted an outsized share of industry flows as a result. Goldman estimates that the total number of employees at these funds has jumped from 5,100 in 2017 to ~24,000 in 2025, collective AUM is now approximately $425 billion – and because these platforms use substantial leverage, multi-managers represent ~37% of hedge fund trading volume despite being only ~10% of industry AUM.

Charlie McElligott, the head strategist at Nomura, described this change the February 6th, 2026 episode of Odd Lots:

"If you look back on the last five to ten years of dollar flows into the hedge fund space, with regards to all new flows: multi-strats are conservatively eighty cents of every dollar in. And if you actually include outflows from other strategies, you're legitimately through one dollar.”

The structural consequence is significant. Within these platforms, stop-losses are tight – down ~2%, and positions get cut. The time horizon for many pod managers is a few weeks to three months. They are attempting to extract basis points of alpha and levering it up, not making multi-year fundamental bets.

Sandler on the Masters in Business podcast, describing the behavior of the multi-manager:

"On top of 'I'm moving to where the narrative is,' I also know that even if that narrative isn't what I believe, if my P&L starts to do something that triggers me to act, I de-risk, I de-lever. So you have, on top of people investing in ways that are narrative-driven, investors who are also backward-looking to their own P&L. If I have a bad month, I might have to do something differently. And I'm telling you, all the stock prices are moving for non-fundamental reasons."

McElligott explained the mechanical dynamics that amplify these moves; systematic strategies and market structure create self-reinforcing momentum in both directions:

"Buying largely feeds momentum. You're not scaling out of positions – the more they trend, you're loading into them. Whether it's target volatility or CTA, you assign an exposure target, a leverage target. If the realized vol is five and your vol target is ten, you've got to lever that two times. Ironically, the lower vol goes, the more you need to add leverage onto that position to match your target. And that's the problem. We create crashes because anyone on a VaR model is actually a momentum trader. You have to deleverage when vol goes higher."

The end result is that among the remaining fundamental investor universe, an increasingly large portion is not volatility-tolerant due to the nature of their product structure… in the meantime the very structure of their product (and the risk-seeking nature of other market participants) is creating the preconditions for large "degrossing" events (a.k.a. forced selling).

These dynamics are likely responsible for the abnormal trading activity we've seen throughout February.

McElligott:

"If you look at a snapshot of a model risk parity portfolio – four assets, long only, using leverage to allocate your volatility across equities, bonds, credit, and commodities – we're seeing, on a five-year lookback, 99.7th percentile gross exposure. And it just so happens: Goldman Sachs prime brokerage data with regards to equity hedge fund grosses, as of last Friday – 100th percentile on a five-year lookback. These are synonymous... the grosses were too damn big… We don't see the 'correlation-one' events anymore – the ones where things shock and everything moves together, down together. That was kind of the old state of the world. But now what we tend to see is something different... The dollars and the leverage controlled by the market-neutral multi-strat equity space are so overwhelming that when you are forced to de-risk or de-gross because the tilts go wrong, you have the offsetting short on the other end. It's not just that you stop out of your net longs or your crowded longs – you're also, theoretically, covering an equal dollar amount on the short side… On the two big down days this week — about 250 stocks were up, 250 stocks were down. So you're getting this reverse dispersion, very much the opposite of what last year was, which was this crazy concentration of top decile versus bottom decile spread — 99th percentile on a ten-year basis… This is why the current environment feels so disorienting. The same structural forces that produced hyper-concentration on the way up produce violent factor rotation on the way down. But because correlation stays low – longs are being sold while shorts are being covered simultaneously – the VIX doesn't spike the way it used to… You need correlation as an input to sustain higher vol, and you're just not getting that. Massive single-stock volatility, enormous factor rotations, but no traditional index-level "crash" signal. The index stays near highs while the median stock experience is far more painful.”

The Reduction of Independent Thought (“The Social Media-fication Of Investing”)

While the three aforementioned trends are resulting in fewer long-term fundamental equity investors as a percent of assets/volumes, I believe the “social media-fication” of investing has impacted all market participants.

The wisdom of crowds, which any functioning market depends on, requires independence among participants. On Odd Lots, Asness used the game show Who Wants to Be a Millionaire to illustrate why this matters:

"My favorite example... is Regis Philbin and Who Wants to Be a Millionaire. You had multiple cheats. One was 'phone a friend,' which was almost useless. A friend usually wasn't much smarter than you, and people seemed to choose friends who knew the same stuff they knew.

The other one was poll the audience. And at least to my non-exhaustive examination, it seemed to work pretty much every time, even if the question was hard. Because imagine you have a hundred people in a room. Ten of them know the answer; the other ones are guessing. The ninety distribute roughly evenly over the four choices. The ten all land on B. So you pick B because it's bigger. Works pretty much every time…

There's a crucial assumption in that: the audience has to be relatively independent of each other. And they were – they weren't talking. It was silent voting. If the audience all gets to talk, maybe the ten convince the ninety, but maybe they don't. Maybe a demagogue with a better Twitter feed convinces everyone. And if you ruin the independence – have we ever come up with a better vehicle for turning a wisdom of crowds into a craziness of mobs than social media? I'd be hard-pressed to describe one."

The classic classroom demonstration of crowd wisdom involves asking a large group to independently estimate something – like Joel Greenblatt’s story of asking his students to estimate the number of jelly beans in a jar. When participants write down their guesses privately, the average tends to be remarkably accurate. But when guesses are announced one by one – allowing each person to hear what others have said – the estimates become correlated, biased by anchoring and social influence, and the aggregate answer drifts far from reality. Once independence is lost, individual errors no longer cancel out – they tend to compound.

I don’t think it’s a stretch to believe that this is what social media does to markets (to at least some degree) at scale. When a narrower set of shorter duration market participants are consuming the same Twitter/X threads, blog posts, and podcast episodes, the diversity of opinion that makes markets function is hampered. The result is a market that is not just less efficient in the traditional sense of mispricing individual securities – it is likely structurally more prone to herding, to narrative-driven momentum, and to violent reversals (exactly what we are seeing).

What This Means

Below are some of my takeaways:

- Short-Term Price Action Has Likely Become Less Relevant

One practical implication is that short-term price action likely carries far less informational content than it once did. We consistently see large daily swings in multi-billion (and trillion) dollar businesses, and post-earnings sell-offs often occur on minor misses (that, in a different regime, would’ve indicated there was something concerning going on with the core business). It used to be that if a stock was off ~7% on earnings, there was virtually a 100% chance you’d end up needing to tweak your numbers lower in your model – but now, I sometimes find myself not revising my numbers downwards (or even nudging my numbers cautiously upwards) before double checking consensus revisions (to confirm I’m not missing something), only to find that consensus is unchanged/higher as well. The narrative is often more important than the numbers over shorter timeframes.

Sandler discussed noticing this increased stock volatility and asking his quant team to dig into it. Their takeaways:

"Implication number one: price action is much more meaningless than we used to think. Call it the one-week to two-to-three-month price action – stocks were acting weirdly and it meant nothing. In the old days, when a stock was acting poorly, you'd think, 'Somebody knows something,' and there was a good amount of time where that company disappointed and you felt at a disadvantage.. The practical response is not to abandon positions but to lean into the volatility. This isn't us turning into traders around the quarters. This is us trimming when something is up 30% for no reason we can identify, buying more when it's down 30% for no reason we can identify."

- Expect Persistent Mispricings, Deviating Further from What We Think Is “Rational”

The HALO trade is Exhibit A. When Industrials trade at 27.5x (100th percentile) and Microsoft trades below Exxon on a forward P/E basis, the market is likely not carefully weighing out the likely future cash flows for these businesses based on a measured assessment of their competitive advantages (i.e. ability to earn outsized returns on capital for a certain duration) and discounting these cash flows back to the present using an appropriate discount rate.

It’s feel more like a thematic rotation where people can’t afford to look wrong over a shorter time period. These phenomenon may very well persist (and even widen) because the structural forces producing them – passive flows, momentum-chasing, narrative-driven retail, levered investors who can’t stomach volatility – are self-reinforcing in the short term.

- The Difficulty Level Increases; But Returns & Opportunities Increase Proportionally

The asymmetry in earnings reactions (beats rewarded modestly, misses destroyed), the violence of factor rotations, and the sheer speed of thematic sell-offs all make it psychologically and practically more difficult to maintain conviction in fundamental positions. The magnitude and speed of the sell-offs in some of the businesses I follow is surprising. I take very little comfort knowing firms I respect, with a similar style to mine, like Akre, Pershing Square, AltaRock , and TCI are down 16%/12%/~9%/~7% on an absolute basis YTD – but ultimately, experiencing losing money is a painful experience that isn’t diluted by having stylistically similar “company.”

However, a less efficient market is, by definition, a more rewarding one for those who can maintain a long-term orientation and take advantage of the resultant mispricing.

The mispricings will almost certainly be larger. Fewer participants are willing to do the work, embrace ambiguity, or deal in nuance. The path forward is almost certainly to embrace the volatility. If stocks, which are simply fractional shares of enterprises, are increasingly going to swing significantly for non-fundamental (or even not-fully-fundamental) reasons, I think investors need to be comfortable with it, and need to lean into it when prudent (selling into abnormal strength, buying into tenuously explained weakness, and understanding they are unlikely to bottom/top-tick names when they do so).

Asness frames the tension; a less efficient market means the expected payoff for rational, patient investing is higher, but the path to capturing that payoff is harder. Bigger ups and downs, lasting longer, requiring more conviction to hold through:

"If there are big deviations from fair value – if you can stick with your positions – not a small thing – you will make money. There are opportunities. And in fact, I think a less efficient market in that sense almost has to deliver bigger opportunities for people who can stick with it. It also makes it considerably harder to stick with, because the extremes you have to live through, and the length of time those extremes can go on... It's a bigger opportunity for people who can stick with it, and it's harder to do. And I find that really fair: harder to do, but more lucrative if you can do it."

My personal response to the above is to maintain a long-term orientation, to focus on the competitive positioning of the businesses I own, and to try and reasonably estimate how much cash they’ll produce in the coming years compared to the current market prices. Ultimately, businesses are cash in (price paid), cash out (free cash flow) machines. I think the likelihood of long-term outperformance has increased for investors who have the stomach and time-horizon to take advantage of an increasingly volatile market.

I am confident in the competitive positioning of the businesses I own, I believe they collectively trade at attractive prices relative to the amount of cash they are likely to produce, and I'm comfortable with the management teams sitting on top of them. It's been a while since I was forecasting IRRs this high across my portfolio. I'm busy using this sell-off in high quality businesses to accumulate shares at attractive prices.

Ultimately, I’m reminded of Ben Graham’s teaching that “Mr. Market is there to serve you, not to guide you. It is his pocketbook, not his wisdom, that you will find useful.”

Disclaimer: Nothing here is investment, legal, tax, or financial advice. It’s opinion for educational purposes only—not a recommendation to buy or sell any security. I may hold positions in securities mentioned and may change them at any time without notice. All discussion regarding investments is in sole reference to my personal investment accounts. Any discussion of performance refers solely to my personal investment accounts, is unaudited and incomplete, and is provided for illustration only. It is not marketing, advertising, or a solicitation for any advisory service, fund, or security. Past performance is not indicative of future results. Do your own research.